Fueling the Hearth: The Economic Friction and Logistical Hurdles of India’s Biogas vs. LPG Transition

We are sitting squarely in the second quarter of the 2026–27 fiscal year, and the real, unvarnished cost of cooking in India is finally hitting home. Look at the math: a 19 kg commercial LPG cylinder currently commands roughly INR 3,000 (about INR 160 a kilo). Strip away the safety net, and a standard 14.2 kg domestic cylinder should realistically retail at nearly INR 2,260. For decades, though, the state kept this economic reality at bay.

But those cushions are rotting away. Under the current fiscal regime, the retail price for household cylinders has climbed to INR 1,155. This slow-motion price shock exposes the friction at the heart of India’s green energy ambitions. Decentralized biogas looks like a brilliant shield against volatile, import-reliant fossil fuel chains. Yet, it is being forced to run a race on an aggressively tilted track.

The debate has shifted. It is no longer a high-minded argument about saving the planet; it is a gritty question of logistical survival. Can biogas actually scale to feed India’s kitchens, or will seasonal bottlenecks and infrastructural gaps keep it permanently cornered as a niche local experiment?

The Subsidy Paradox and the 2026 Fiscal Pivot

Subsidizing fossil fuels does more than just coddle consumers; it actively hides the true return on investment for clean alternatives. If domestic LPG were sold at its true economic weight of over INR 2,000, the payback period for a household biogas digester would instantly shrink to just 15 to 18 months.

Instead, we are watching a forced economic re-alignment. The Union Budget 2026–27 has shown a decisive 27% reduction in the LPG subsidy pool—slashing it to INR 11,085 crore from the previous year’s revised estimate of INR 15,121 crore. To sweeten the deal for green alternatives, the government has wiped out the central excise duty on compressed biogas (CBG) blended with CNG. It is a loud, deliberate policy nudge away from imported crude.

Key Takeaway: The economic viability of biogas has long been artificially suppressed by fossil fuel subsidies. As fiscal policies shift and LPG subsidies are systematically dismantled, the economic argument for localized biogas becomes increasingly undeniable.

Comparative Snapshot: LPG vs. Biogas (2026 Context)

| Parameter | LPG (Liquefied Petroleum Gas) | Biogas / Bio-LPG |

|---|---|---|

| Source & Supply | Fossil-fuel-derived; heavily import-dependent (around 60%) and highly centralized. | Harvested locally from organic waste, pressmud, and crop residues. |

| Price Volatility | High; closely pegged to global crude swings and Saudi Aramco contract prices. | Low; fueled by local feedstocks, shielding it from global supply shocks. |

| Household Payback | N/A (A perpetual, recurring operational expense). | 2 to 4 years (shrinking fast as household LPG prices climb). |

| Commercial Payback | N/A (Substantial, permanent monthly operating expenditure). | 4 to 8 years (shaving off 50% to 80% of commercial fuel overheads). |

| Infrastructure Fit | Turnkey compatibility; taps into India’s massive, well-oiled national cylinder distribution network. | Dual path: Needs dedicated local pipes/burners for raw gas, or upgrading to Bio-LPG for drop-in cylinder fit. |

The Bridge: Infrastructure Fit and the Bio-LPG Distinction

As the “Infrastructure Fit” column in our matrix suggests, the final battle for these gaseous fuels is won or lost at the kitchen stove. It is a matter of plumbing. Here, we must draw a hard line between raw biogas, Compressed Biogas (CBG), and Bio-LPG.

Raw biogas and CBG do wonders for localized power grids or captive vehicle fleets, but they are terrible direct replacements for the standard domestic LPG cylinder. CBG requires heavy, high-pressure storage tanks and entirely different burner configurations.

Enter Bio-LPG—the undisputed holy grail of this transition. Chemically indistinguishable from conventional propane and butane but brewed from plant-based lipids and organic waste, it is a genuine “drop-in” fuel. It can flow through India’s massive, pre-existing three-tier bottling and distribution network without forcing a single family to buy a new stove, or requiring municipal bodies to tear up streets for pipelines.

Right now, policymakers are scrambling to build out pathways to scale Bio-LPG. But because commercial-scale refining of Bio-LPG is still in its absolute infancy, the immediate heavy lifting falls back on raw biogas and localized CBG. This brings us face-to-face with the messy, physical reality of gathering agricultural waste.

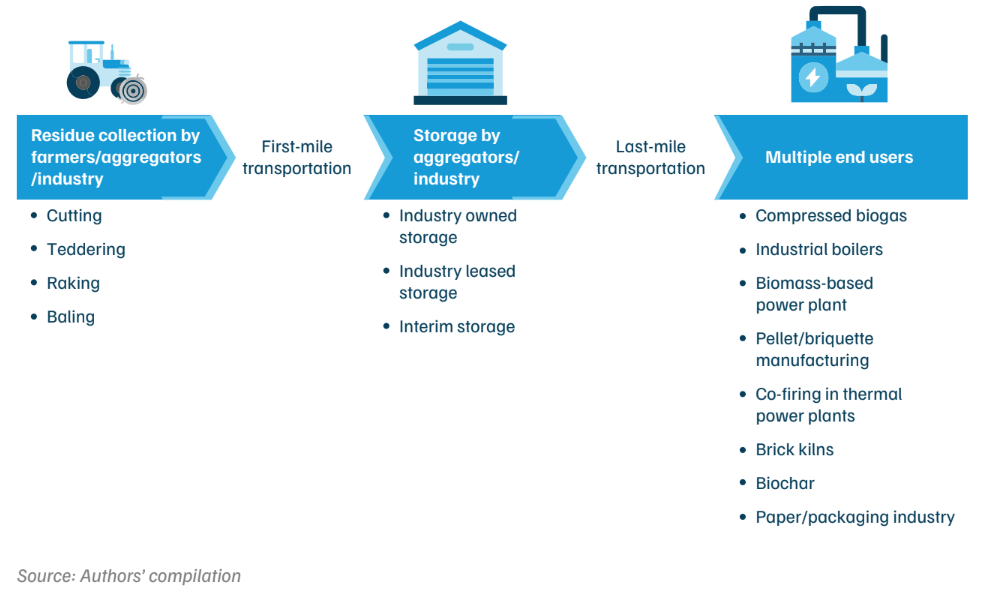

The Logistics Conundrum: Why Biomass Struggles to Scale

The bottleneck preventing biogas from dethroning LPG across India is not the science of anaerobic digestion. The real villain is the chaotic, highly fragmented state of Biomass Supply Chain Management (SCM). Unlike centralized fossil fuels, crop residue is seasonal, scattered across millions of small farms, and incredibly difficult to move.

- Storage and Financial Leakage: Just try storing 6 million metric tonnes (MMT) of paddy straw to keep utility-scale CBG plants running year-round. It requires an immediate infrastructure spend of INR 150 to 240 crore. That translates to an upfront storage tax of INR 250 to 400 per tonne depending on whether you are handling rectangular or round bales. If you do not lock this down, the feedstock rots in the rain, loses its energy density, and bleeds cash for the developers.

- The Workforce Gap: The sudden rush to build bioenergy plants has triggered a massive talent deficit. Instead of training new operators, companies are poaching from one another. To break this logjam, the government has launched specialized Skill India bio-energy certifications. The goal is to standardize operations for digesters and logistics, though the talent pool remains critically tight for now.

- The Tech Gap in the Supply Chain: Today’s digital biomass marketplaces are mostly glorified classifieds. They lack the real-time, localized logistics networks needed to balance highly seasonal farm harvests with the steady, 365-day appetite of a commercial refinery. This leaves both farmers and plant operators at the mercy of wild price swings during harvest windows.

Micro-Successes vs. Macro-Struggles

While massive, centralized plants trip over supply chain issues, tiny, hyper-local projects are thriving by opting out of the national supply chain altogether.

In May 2026, a major milestone was reached near the Statue of Unity in Ekta Nagar, Gujarat, where nearly 1,000 tribal households began taking their energy security into their own hands. More than 600 domestic biogas plants are up and running, funded entirely by a 100% government subsidy initiative. By mixing just 10 kg of cow dung with 90 kg of water every day, these families produce enough clean gas to save about two LPG cylinders per month.

Even better, the math for these rural families is getting an assist from India’s developing domestic carbon market (ICM). Local cooperatives running these digesters are starting to bundle carbon offsets, turning avoided methane emissions into hard cash. This secondary revenue stream pays for maintenance and keeps the systems running. Meanwhile, in urban neighborhoods across Kerala and Mumbai, the sting of high LPG prices has forced residential associations to dust off and upgrade their old, dormant food-waste digesters.

On the macro scale, the transition is pushing forward along a parallel track, driven by the Sustainable Alternative Towards Affordable Transportation (SATAT) program. With fresh policy mandates pushing for CBG blending in city gas pipelines, the Ministry of New and Renewable Energy (MNRE) has cleared 94 bio-CNG/CBG projects, backing them with INR 90.89 crore in central financial assistance. State-backed giants are jumping in too, highlighted by HPCL’s massive USD 231 million investment to build 24 compressed biogas plants across the country.

Even with these wins, expecting biogas to completely replace LPG tomorrow is a fantasy. As we navigate the rest of 2026, the transition looks less like a clean break and more like a pragmatic compromise. Biogas is proving itself as an invaluable local hedge against energy volatility, while conventional LPG continues to run heavy industrial hubs and dense urban kitchens. In the end, the winner of India’s clean cooking race won’t just be the cleanest molecule—it will be the system that successfully tames the chaotic economics of the rural Indian countryside.

Summary of Key Insights

- Subsidy Realignment: A sharp 27% slash in LPG subsidies has driven retail prices to INR 1,155, making biogas economically competitive.

- Logistical Bottlenecks: Unstable seasonal biomass supply chains and high storage costs (INR 250–400/tonne) continue to block large-scale macro adoption.

- Decentralized Viability: Local micro-projects, fueled by carbon credits under India’s emerging domestic market, are successfully delivering rural energy independence.