The Hydrogen Paradox: Thermodynamics, Industrial Realism, and India’s Path to Decarbonization

Thermodynamics is a cold, unforgiving mistress. For enthusiasts of Green Hydrogen (GH2), she offers a particularly bitter pill to swallow. While the vision of “water-powered” fleets captures the public’s imagination like a mid-century sci-fi novel, the physics of energy conversion tells a far more cynical story. Transforming renewable electrons into hydrogen via electrolysis, squeezing it under immense pressure, hauling it across distances, and finally forcing it back into electricity via a fuel cell is an exercise in profound waste. When direct electrification boasts 80-90% efficiency, the ~30% round-trip efficiency of hydrogen for light vehicles isn’t just a technical “bug”—it’s a massive economic tax on every kilometer traveled.

To navigate this landscape, we have to strip away the marketing and look at the molecular reality. Grey Hydrogen, the dirty incumbent, is ripped from natural gas through steam methane reforming, belching CO₂ into the atmosphere as a byproduct. Green Hydrogen, conversely, is the product of splitting water using renewable power, leaving only oxygen behind. It is the undisputed holy grail of deep decarbonization. Yet, if we spray this precious resource on sectors where batteries already dominate, we risk squandering the very renewable energy we are trying to save.

The Efficiency Chasm: Electrification vs. Hydrogen

The shouting match over hydrogen transport often glosses over the “well-to-wheel” disaster of energy loss. Direct electrification is the apex predator of land-based transit. Hydrogen, by contrast, is a niche player, relevant only where the sheer mass of batteries hits a wall of diminishing returns.

| Feature | Direct Electrification (Rail/EV) | Green Hydrogen (FCEV) |

|---|---|---|

| Cycle Efficiency | 80% – 90% | ~30% – 35% |

| Primary Infrastructure | Existing Grid / Overhead Lines | High-pressure Refueling / Cryogenic Storage |

| Optimal Use Case | High-density routes, Light vehicles | Hard-to-abate heavy industry, Shipping |

| Cost Maturity | High (Declining Battery Costs) | Low (High CAPEX for Electrolyzers) |

| Thermodynamic Loss | Minimal (Transmission/Battery) | Massive (Electrolysis/Liquefaction/Heat) |

This efficiency chasm is widened by brutal economic realities. To hit the target price of $1.56/kg by 2028, three stars must align: renewable energy costs must crater, electrolyzer manufacturing must scale to a massive degree, and operational loads must be perfectly optimized. Without this trifecta, GH2 remains a boutique fuel for sectors where batteries are simply “not enough.”

The “Hard-to-Abate” Necessity

If the physics are so punishing, why is the world obsessed? Because for some industries, electrons alone are useless. Steel manufacturing, oil refining, and fertilizer production aren’t just energy hogs; they are chemically tethered to hydrogen. In a blast furnace, hydrogen acts as a surgical tool, stripping oxygen from iron ore. In a fertilizer plant, it’s the literal backbone of ammonia. These are processes that require intense, high-grade heat and molecular feedstocks that a lithium-ion battery cannot replicate.

The consensus among the realists is blunt:

“Put the money where the demand is. Green hydrogen is not a universal fuel; it is a surgical tool for decarbonizing industrial giants that are otherwise impossible to clean.”

A deep dive by Bain & Company and RMI suggests that 64% to 78% of GH2 demand by 2030 will be hyper-local, centered around industrial clusters. The strategy is shifting: forget the hydrogen-powered sedan. The real win is swapping “Grey” molecules for “Green” ones inside the massive, existing industrial loops that keep the modern world spinning.

India’s Ambition vs. Ground Reality

The National Green Hydrogen Mission is India’s biggest energy bet yet, aiming for a staggering 5 MMT per annum by 2030. But the bridge between a government press release and a functioning plant is currently a rickety one.

- The Implementation Gap: By early 2026, India’s actual commissioned capacity sat at roughly 8,000 tonnes per annum (TPA). While paper announcements exceed the 5 MMT target by 2.5x, the “gold standard” of bankability—binding offtake agreements—remains frustratingly rare.

- The Water Constraint: Electrolysis is a thirsty business. It devours nine liters of ultra-pure water for every kilogram of hydrogen. In a nation where water security is a zero-sum game, finding the right spot for a GH2 hub means balancing high solar yields against local hydrological survival.

- Safety and Handling: Hydrogen is the escape artist of the periodic table. Its tiny molecules leak through the smallest gaps and can turn standard steel pipes brittle. Managing these risks in a controlled plant is one thing; building a national “hydrogen grid” is an engineering nightmare that adds layers of hidden costs.

The Global Retreat and Strategic Risks

The initial “Hydrogen Hype” is currently meeting its “Morning After.” Giants like BP and Origin Energy have recently tapped the brakes on major projects, spooked by cost spikes of up to 65%. Across the Atlantic, the cancellation of major hydrogen hub orders proves that “build it and they will come” is not a viable energy policy. The market is demanding certainty, not just subsidies.

For India, there is a looming danger of grid cannibalization. If we divert massive amounts of wind and solar to produce an inefficient fuel for transport, we might starve the general grid. The irony would be painful: electric vehicles running on coal-fired power because all the “clean” electrons were busy being turned into expensive hydrogen for experiments that don’t scale.

Unlocking the Demand: A Five-Pronged Strategy

Transitioning from pilot projects to a 5 MMT powerhouse requires more than just supply-side hope. RMI and CII point toward five levers to force the market’s hand:

- Mandatory Blending: Force the issue. Set strict, escalating quotas for GH2 in refineries and fertilizer plants to create an artificial, yet necessary, floor for demand.

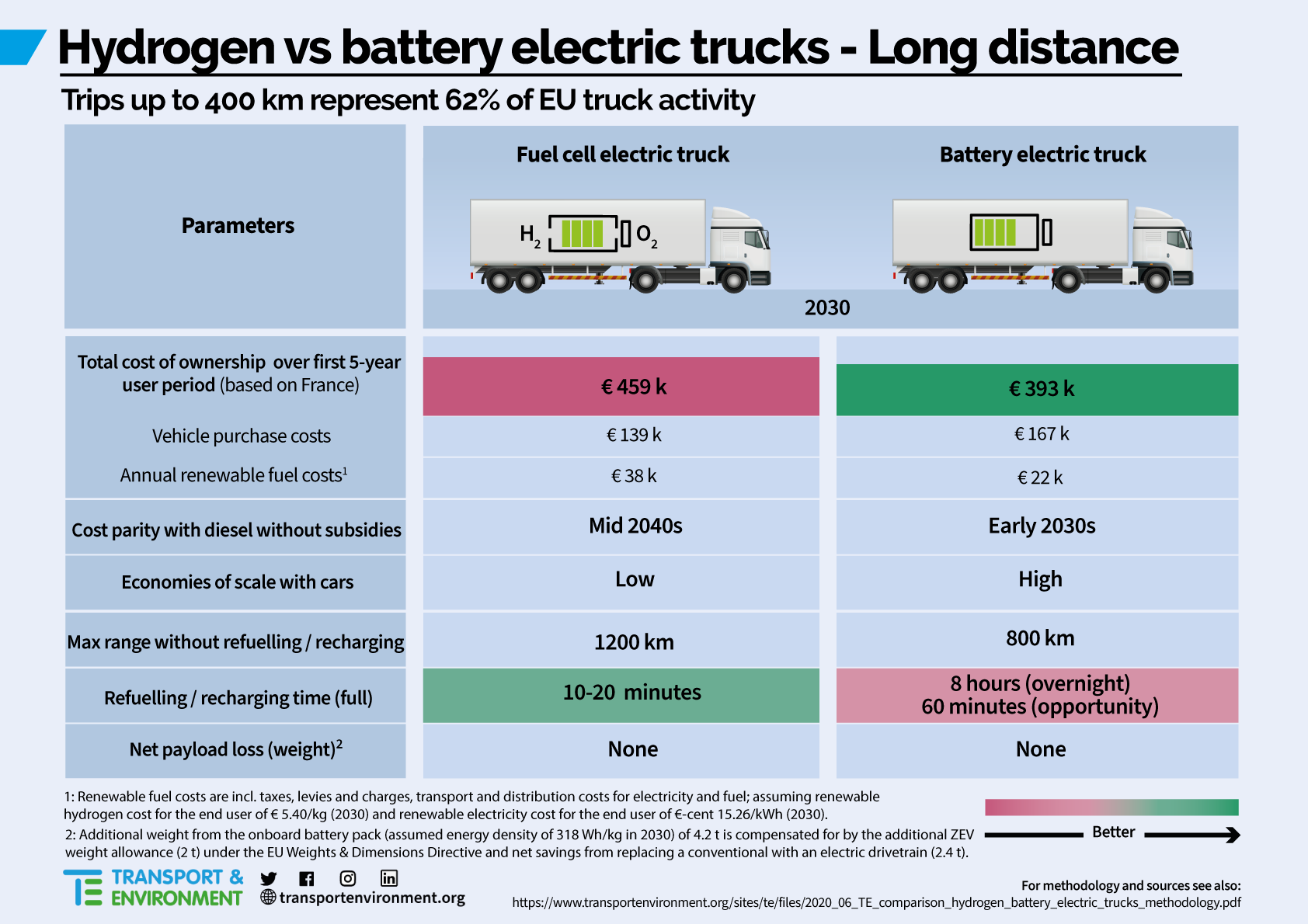

- Niche Substitution: Stop chasing passenger cars. Focus transport dollars on heavy-duty, long-haul trucking and maritime shipping—territories where batteries weigh too much to work.

- Green Procurement: The government must lead. Mandate “green steel” for bridges, railways, and highways to create a high-value market for low-carbon materials.

- Export Hubs: India has some of the cheapest solar on Earth. We should be exporting Green Ammonia—which is far easier to ship than gas—to energy-starved markets.

- Value-Added Exports: Don’t just ship the raw gas. Move up the chain by exporting finished “green” products, like DRI steel, capturing the premium that the world is willing to pay for decarbonized industrial goods.

Summary: The Path Forward

“• Hydrogen’s poor thermodynamic efficiency relegates it to a secondary role behind direct electrification for light-duty mobility.” “• Success depends on prioritizing ‘hard-to-abate’ heavy industries—steel and chemicals—where hydrogen serves as a vital, irreplaceable chemical feedstock.” “• India must bridge the gap between ambitious 5 MMT targets and actual infrastructure, solving for water scarcity and infrastructure safety.”