The Atomic Cloud: Silicon Valley’s Nuclear Pivot and the Quest for 24/7 Power

Silicon Valley’s new arms race isn’t happening in the pristine clean rooms of chip fabs or the quiet hum of software labs. It is a brawling, desperate scramble for raw, unadulterated electricity. For over a decade, the “Big Five”—Google, Microsoft, Amazon, Meta, and Apple—headlined the global transition to green energy, buying up wind and solar capacity at a scale the world had never seen. But the math has changed. As the generative AI fever pushes data center energy consumption toward a staggering 1,300 terawatt-hours (TWh) by 2035 (source: Goldman Sachs), the physics of intermittency has finally hit a wall.

To meet the staggering energy demands of the generative AI boom, tech giants are shifting from being mere consumers of electricity to becoming independent power producers. These companies are now building their own fleets of private power plants to ensure their data centers remain operational 24/7.

The Natural Gas Bridge and Net-Zero Risks

While the “Big Five” (Google, Microsoft, Amazon, Meta, and Apple) have long championed renewable energy, the immediate need for massive, reliable power has forced a pragmatic—and controversial—shift. Most of these newly constructed private power plants are currently fueled by natural gas.

This reliance on fossil fuels creates a significant conflict with corporate sustainability mandates. By integrating gas-fired generation into their private infrastructure, tech companies are actively risking their net-zero goals, as the carbon emissions from these plants threaten to offset years of investment in wind and solar.

Nuclear: The Long-Term Solution for Dispatchable CFE

The industry recognizes that natural gas is an unsustainable bridge. As a result, Silicon Valley is pivoting toward nuclear energy as the essential long-term provider of Carbon-Free Energy (CFE).

Unlike intermittent sources like wind and solar, nuclear power is “dispatchable”—it can be adjusted to meet demand and provides a constant baseload of electricity. For tech companies, nuclear represents the only viable way to secure a 24/7 power supply that can support AI growth without abandoning their climate commitments.

The 24/7 Carbon-Free Energy (CFE) Paradox

Most tech leaders checked the “100% renewable” box years ago, but that victory was largely an accounting trick rather than a physical reality. Companies leaned on Renewable Energy Certificates (RECs) and annual Power Purchase Agreements (PPAs) to balance their books. In the real world, when the sun dips below the horizon and the wind stalls, these data centers are still sucking down “gray” electrons from gas-heavy grids.

The new gold standard is 24/7 Carbon-Free Energy (CFE)—a gritty commitment to match every single hour of consumption with carbon-free production on the exact same local grid. For a facility running H100 GPUs at 100% utilization, the volatility of weather-dependent power is no longer a quirk; it’s a liability.

“Nuclear energy is no longer a ‘plan B’; it is becoming the foundational baseload for the AI era. Without a dispatchable, zero-carbon source, the net-zero targets of 2030 and 2040 are mathematically impossible under current AI growth trajectories.”

Comparing the “Nuclear Footprint” of Tech Giants

| Company | Current Renewable Status | Nuclear Strategy & Key Deals | Stance on Nuclear |

|---|---|---|---|

| Microsoft | 100% by 2025 (target) | 20-year deal with Constellation Energy to resurrect Three Mile Island (Unit 1). | Proponent: Essential for carbon-negative 2030 goal; also invested in Helion (Fusion). |

| 100% since 2017 | World’s first corporate SMR deal with Kairos Power; targeting 500MW by 2030. | Proponent: Nuclear provides the “firm” power that wind/solar lack. | |

| Amazon | 100% since 2023 | $500M investment in X-energy; purchased Cumulus Data Center powered by Talen Energy’s nuclear plant. | Proponent: Scalable CFE is the only way to meet “The Climate Pledge.” |

| Meta | 100% since 2020 | Seeking 1–4 GW of nuclear capacity; exploring partnerships with Sage Geosystems and SMR providers. | Proponent: Openly seeking nuclear RFPs to decarbonize its global AI infrastructure. |

| Apple | 100% since 2018 | No active nuclear investments; focused on solar, wind, and massive battery storage. | Skeptic: Prioritizes “strictly renewable” sources; cites waste and safety concerns. |

The Apple Anomaly: Apple’s refusal to label nuclear as “clean energy” is a stubborn holdover from California’s specific brand of environmentalism. By doubling down on “additionality”—the act of bringing entirely new renewable projects onto the grid rather than buying existing nuclear output—Apple sidesteps the political baggage and long-term waste liabilities that come with fission.

The Silicon Bottleneck: Why Renewables Aren’t Enough

The explosion of AI has fundamentally broken the old demand curves. The International Energy Agency (IEA) now expects global data centers to swallow roughly 3% to 4.4% of all global electricity by 2030. In the U.S. alone, the Electric Power Research Institute (EPRI) warns that demand will scream toward 130 GW (1,050 TWh) by the end of the decade.

- Intermittency vs. Uptime: Data centers demand “five-nines” (99.999%) reliability. Solar and wind are cheap per MWh, but they are fickle. Nuclear offers a 90%+ capacity factor, the highest reliability of any energy source on the planet.

- The Land Constraint: Sprawling a 1-GW data center campus across the landscape would require 4,000–6,000 acres of solar panels. A Small Modular Reactor (SMR) can churn out that same power on a footprint smaller than 100 acres.

- Grid Congestion: In hubs like Northern Virginia, utilities are choking on a decade-long backlog of interconnection requests. By “bringing their own power” (BYOP) through private nuclear fleets or co-locating directly at existing plants, tech giants are effectively cutting to the front of the line.

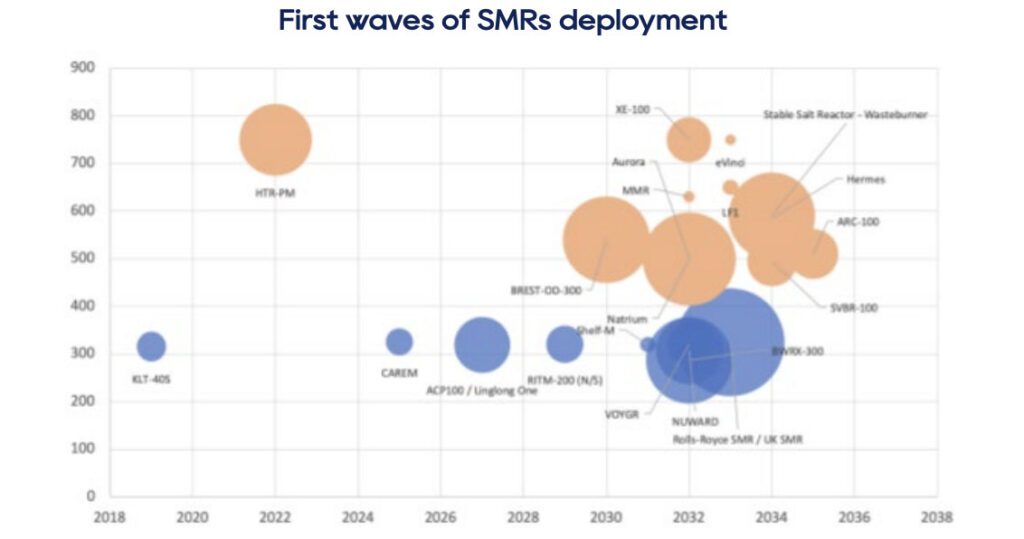

The Rise of the SMR: Small, Modular, and Strategic

The industry is placing a massive bet on Small Modular Reactors (SMRs). Forget the traditional gigawatt-scale behemoths like Georgia’s Vogtle, which took 15 years and $30B+ to complete. SMRs are built for factory assembly and rapid, cookie-cutter deployment.

- The Reliability Tax: The median Levelized Cost of Electricity (LCOE) for SMRs sits at roughly $77.71/MWh (source: NEA), dwarfing utility-scale solar at ~$32/MWh. For Big Tech, this isn’t a cost—it’s a “reliability tax” they are more than happy to pay to ensure their multi-billion dollar AI clusters never flicker.

- The Regulatory and Public Hurdle: Even with the hype, the SMR path is riddled with friction. The U.S. Nuclear Regulatory Commission (NRC) moves at a glacial pace, and “NIMBY” (Not In My Backyard) sentiment is a constant shadow. While SMRs produce less waste by volume, the back-end waste management of spent fuel remains a political lightning rod. The NEA is pushing for deep geological repositories, following Finland’s Onkalo model, to finally solve the permanent storage puzzle.

Beyond Fission: The Search for 24/7 Alternatives

Nuclear fission is the clear frontrunner, but it isn’t the only horse in the race for firm, zero-carbon power. Microsoft has already inked a power purchase agreement with Helion Energy for fusion power by 2028—a timeline many physicists dismiss as “aspirational.” Others are betting on Enhanced Geothermal Systems (EGS), using fracking techniques to tap the earth’s internal furnace, or Long-Duration Energy Storage (LDES) like iron-air batteries. So far, however, nothing matches the sheer energy density and maturity of fission.

The Indian Context: A Nuclear Inevitability

The pivot toward SMRs is playing out even more dramatically in developing giants like India, where data center consumption is set to double from 9 TWh today to 18 TWh by 2030.

- The Nuclear Mission: The Union Budget 2025–26 carved out ₹20,000 crore for SMR development, a clear signal that the government is moving toward decentralized nuclear power.

- The Policy Shift: Principal Scientific Advisor Ajay Kumar Sood has called nuclear energy “inevitable” for India’s 2070 net-zero goals. As land acquisition for massive solar parks becomes a political nightmare, SMRs are the perfect “focused energy supply” for data center clusters in Maharashtra and Tamil Nadu.

The Geopolitical Imperative

This isn’t just about juice; it’s about security. Right now, 40% of the world’s uranium fuel supply (specifically HALEU—High-Assay Low-Enriched Uranium) is controlled by Russia. The U.S. and its allies are in a dead heat to build a “civil nuclear supply chain” to break that grip. By anchoring these projects with long-term contracts, tech companies are effectively bankrolling the rebirth of Western nuclear manufacturing, shielding the “Atomic Cloud” from future geopolitical shocks.

Strategic Summary

- The Demand Surge: AI’s 1,300 TWh appetite makes solar’s intermittency a liability for constant uptime.

- The Nuclear Pivot: Microsoft, Google, and Amazon are funding SMRs and restarts to bypass gridlocks and secure baseload power.

- The Economic Reality: Despite higher costs ($77/MWh), nuclear’s high capacity factor makes it the only viable solution for the AI-driven “Atomic Cloud.”