Beyond the Mine: The Midstream Smelting Chokehold Redefining Global Sovereignty

𝗧𝗵𝗲 𝗿𝗲𝗮𝗹 𝗰𝗵𝗼𝗸𝗲𝗽𝗼𝗶𝗻𝘁 𝗶𝗻 𝘁𝗵𝗲 𝗥𝗮𝗿𝗲 𝗘𝗮𝗿𝘁𝗵 𝗦𝘂𝗽𝗽𝗹𝘆 𝗶𝘀 𝗻𝗼 𝗹𝗼𝗻𝗴𝗲𝗿 𝗴𝗲𝗼𝗹𝗼𝗴𝗶𝗰𝗮𝗹 𝗿𝗲𝘀𝗲𝗿𝘃𝗲𝘀 𝗯𝘂𝘁 𝘁𝗵𝗲 𝗺𝗶𝗱𝘀𝘁𝗿𝗲𝗮𝗺 𝗶𝗻𝗱𝘂𝘀𝘁𝗿𝗶𝗮𝗹 𝗰𝗶𝗿𝗰𝘂𝗶𝘁𝗿𝘆 𝗼𝗳 𝘀𝗺𝗲𝗹𝘁𝗶𝗻𝗴 𝗮𝗻𝗱 𝗿𝗲𝗳𝗶𝗻𝗶𝗻𝗴 𝗼𝗳 𝗼𝗿𝗲 𝗮𝗻𝗱 𝘀𝗰𝗿𝗮𝗽 𝗶𝗻𝘁𝗼 𝗵𝗶𝗴𝗵-𝗽𝘂𝗿𝗶𝘁𝘆 𝗼𝘅𝗶𝗱𝗲𝘀

We are staring down a ticking clock. The looming expiration of China’s 12-month freeze on expanded rare earth export controls on November 10, 2026, has triggered a quiet panic across Western capitals. When Beijing enacted this suspension in late 2025, naive observers called it a peace offering. It wasn’t. It was a cold, calculated squeeze. By temporarily flooding the global market with dirt-cheap oxides, China artificially cratered prices, effectively suffocating cash-strapped Western midstream startups before they could even get their boots on the ground.

For a decade, Western lawmakers played a naive game of geological hide-and-seek, treating critical mineral security like a simple race to dig holes in the ground. But 2026 has shown us the brutal reality: the real chokehold isn’t who pulls the dirt out of the earth. It is who owns the hyper-complex, punishingly expensive chemical refineries that turn raw ore into high-purity oxides. **This realization has shifted the theater of conflict from the mine site to the refinery floor.

You can find these minerals almost anywhere. But the industrial machinery needed to smelt, separate, and forge them into permanent magnets? That remains locked in a single room.

The Refining Monopoly: China’s Midstream Grip

Talk of immediate decoupling is pure fantasy. The numbers tell a story of total capture. Back in 2024, China mined 59% of global rare earths—a solid majority, but not an absolute monopoly. Yet, they controlled 91% of refining and a jaw-dropping 94% of permanent magnet manufacturing.

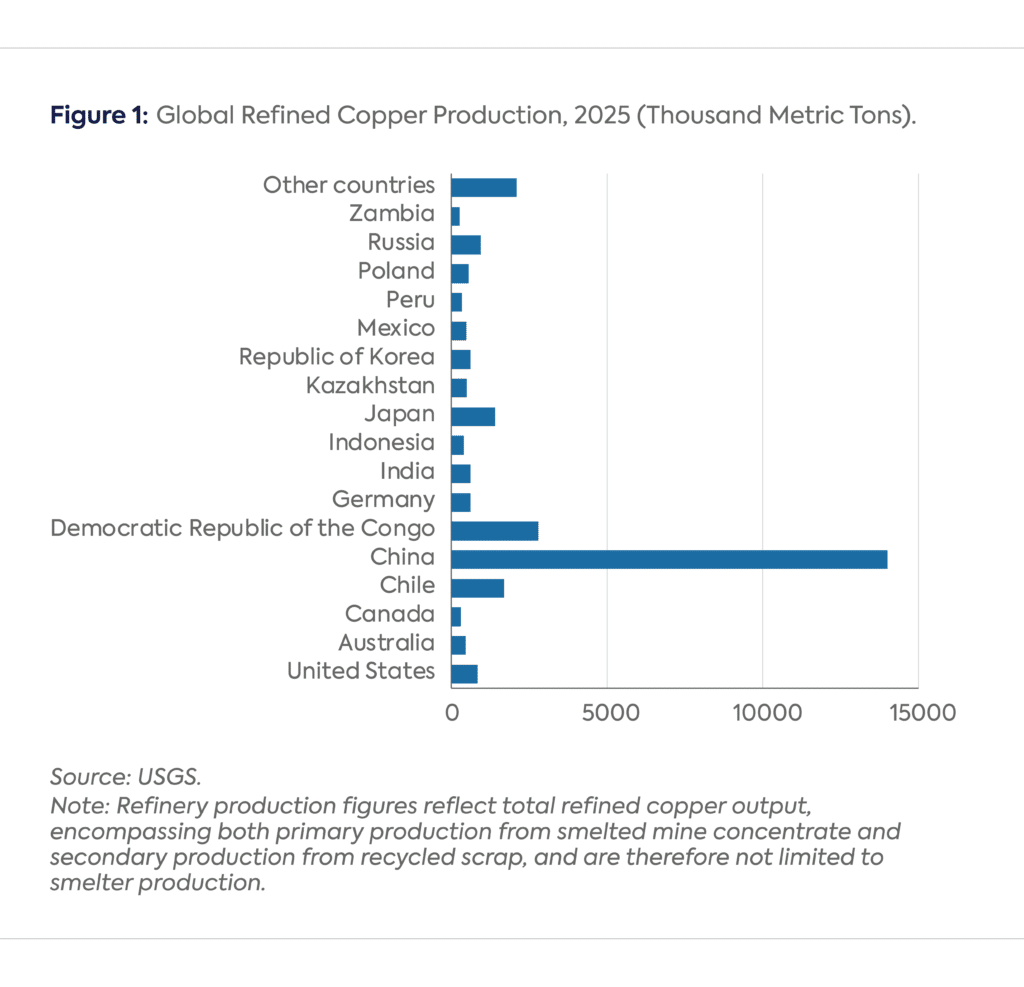

This isn’t just about exotic rare earths either; the same trap has been sprung on workhorse metals like copper. Beijing now commands more than half of the world’s copper smelting and refining capacity. This aggressive concentration of heavy industry has thrown the global copper concentrate market into a tailspin, creating a massive supply-demand imbalance.

Key Takeaway: By aggressively scaling up its domestic smelters, China has systematically crushed global operating margins, sending Treatment and Refining Charges (TC/RCs) into a freefall. This May 2026, Japanese smelting giant Sumitomo Metal Mining conceded that while it hopes to eke out double-digit TC/RCs for the upcoming cycle, these rates will slide far below the 2025 benchmark of $25 per metric ton. It is a stark reminder of the sheer weight of Chinese overcapacity.

This margin squeeze and the tight embargo on processing tech are twin pillars of the same mercantilist strategy. One uses raw economic muscle to starve Western rivals of cash; the other slams the door on the intellectual property needed to fight back. When Beijing banned the export of rare earth processing and separation technologies in 2023, it left Western engineers staring at a blank slate, scrambling to reinvent highly toxic, incredibly complex solvent extraction processes from scratch.

We need a heavy dose of realism here. For all the lofty speeches in Washington and Brussels, Western automakers and defense contractors are still quietly hooked on cheap Chinese materials. Shareholders demand protected margins, and when faced with the steep “green premium” of domestic, ESG-compliant refining, corporations balk. Without massive, permanent government subsidies, they simply won’t buy Western.

The Western Counter-Offensive: Capital and Chemistry

To break this stranglehold, Western allies are throwing both capital and chemistry at the wall, hoping to leapfrog traditional, toxic refining processes entirely.

1. Disruptive Technology Partnerships

Just days ago, on May 20, 2026, Massachusetts startup Nth Cycle and supply chain developer Ionic Rare Earths (IonicRE) inked a joint licensing deal to deploy modular electro-extraction technology on American soil. It’s a clever move. By ditching the massive, chemical-heavy footprints of traditional solvent extraction, this modular setup offers a cheaper, cleaner path to process rare earths, nickel, cobalt, and copper right at home.

2. Sovereign Wealth and Strategic Financing

- The United States: Washington is shedding its old free-market dogmas, using state-backed capital to buy national security. The U.S. State Department recently moved to pump $250 million into the newly minted Pax Silica Fund, a vehicle created to link raw mineral processing directly to the domestic chipmaking boom.

- Canada: On April 27, 2026, Ottawa officially launched the C$25 billion Canada Strong Fund—its first true sovereign wealth vehicle—with critical minerals positioned squarely in the crosshairs. This massive federal push is mirrored at the provincial level by Ontario’s new $500 million Critical Minerals Processing Fund (CMPF), aimed at keeping local ores from leaving Canadian soil unrefined.

- Australia: Long content with a “dig it up and ship it out” economy, Canberra is pivoting. This May 2026, Australia launched state-of-the-art processing research centers at the Australian Nuclear Science and Technology Organisation (ANSTO) to master domestic, high-value refining.

The Environmental Paradox: Speed vs. Security

Yet, all the money in the world cannot easily navigate the West’s own regulatory maze. This is our great paradox: we want security, but we also want pristine backyards. While Europe’s bureaucratic gridlock is legendary, both Washington and Canberra are finding out that fast-tracking mineral processing is a political minefield.

Take the US, where high-profile midstream projects—like MP Materials’ expansion at Mountain Pass or new refining sites in Texas—are running headfirst into fierce NIMBY resistance. The sticking point? Radioactive waste. Refining rare earths leaves behind nasty byproducts like thorium and uranium, and local communities want no part of it. Australia is hitting the exact same wall. The West is discovering, painfully, that securing its supply chains means making hard, dirty choices about the environmental regulations it loves to preach.

The Non-Aligned Midstream: The Global South’s Pragmatic Leverage

But don’t mistake this for a simple two-player game between Washington and Beijing. Non-aligned powerhouse nations in the Global South are playing their own hands. Refusing to remain mere resource colonies, countries from Southeast Asia to South America are using their geological wealth as leverage to force domestic industrialization.

Look at Indonesia. Jakarta pioneered a brutal, effective brand of resource nationalism in its nickel sector. By banning the export of raw nickel ore, they forced foreign corporations—mostly Chinese, but now increasingly Western—to build advanced High-Pressure Acid Leach (HPAL) plants right on Indonesian soil.

Brazil is pulling a similar move, leveraging its near-monopoly on niobium and its promising new rare earth developments like Serra Verde to market itself as a reliable, non-aligned refining hub. These countries aren’t interested in picking a side in the new Cold War; they are exploiting the panic to capture the highly profitable midstream for themselves. They’ve proved that midstream leverage isn’t just a superpower privilege anymore.

Europe’s Reality Check: Regulatory Ambition vs. Geological Inertia

While North America and Australia make messy progress, Europe remains largely paralyzed by its own high ideals. The EU’s Critical Raw Materials Act (CRMA) sets out grand, non-binding targets for 2030: mining 10% of its own demand and refining 40% of it within European borders.

But a devastating report dropped this May 2026 by the European Court of Auditors has laid bare the fantasy of these goals:

- Protracted Timelines: Planning a mine in Europe takes decades, not years. In Sweden, the bureaucratic slog can drag on for over 30 years.

- Recycling Deficiencies: The EU’s recycling targets are too broad and lack specific mandates for individual elements, meaning nobody is bothering to recover the difficult rare earths locked inside electric vehicle motors.

- High Operational Costs: Sky-high energy prices, red tape, and a lack of steady scrap supplies have left European recycling startups dead in the water, unable to compete globally.

Even amidst this gloom, there are small victories. On April 13, 2026, Neo Performance Materials successfully fired up its heavy rare earth element (HREE) solvent extraction line at its Silmet plant in Estonia. It’s a rare, concrete step forward for a continent desperate for industrial autonomy.

Comparative Analysis of Global Midstream Initiatives

The table below charts how the world’s major players are positioning themselves to break China’s refining monopoly as of May 2026:

| Country / Region | Key Midstream Target | Funding & Policy Vehicles | Recent 2026 Milestone |

|---|---|---|---|

| United States | Complete “mine-to-magnet” domestic defense supply chain by 2027. | Defense Production Act; $250M Pax Silica Fund. | Nth Cycle & IonicRE modular electro-extraction partnership. |

| European Union | 40% domestic processing and 25% recycling by 2030. | Critical Raw Materials Act (CRMA). | Neo Performance Silmet facility HREE line commissioned in Estonia. |

| Canada | Onshore processing of domestic ores via sovereign-backed capital. | C$25B Canada Strong Fund; $500M Ontario CMPF. | Launch of the Canada Strong Fund sovereign wealth vehicle. |

| Australia | 15% to 50% downstream processing of extracted minerals. | National Critical Minerals Strategy. | Opening of new ANSTO processing and refining research facilities. |

| India | Build 5 million tonne strategic stockpile; secure value chains by 2030. | $1.9B National Critical Mineral Mission. | NLC India Q4 FY26 profit surge supporting 1Mt processing target. |

| Indonesia | Establish domestic HPAL nickel refining hub; expand into battery precursor manufacturing. | Nickel export bans; mandatory domestic joint ventures. | Successful scale-up of HPAL facilities processing domestic laterite ores into battery-grade nickel. |

Outlook: The Crucible of the Next Six Months

We are on a collision course with November 10, 2026. The next six months will serve as the ultimate pressure test for Western industrial policy. If Beijing lets its export-control holiday expire and slams the door shut again, the resulting supply shock will immediately test whether these new modular technologies and sovereign funds are ready for prime time.

But there is a silver lining: a sudden shock might be the exact jolt needed to force vehicles like the Pax Silica Fund and the Canada Strong Fund to deploy their capital without delay. Ultimately, the race is on: can the West bridge the vast gulf between its geopolitical ambitions and its agonizingly slow regulatory bureaucracy before China pulls the plug again? We are about to find out.

- China’s refining monopoly endures as cost-conscious Western corporations struggle to abandon cheap imports.

- Bureaucratic red tape and local NIMBYism severely stall Western attempts to scale domestic processing.

- Pragmatic, non-aligned nations leverage raw materials to build their own profitable, independent midstream hubs.