The Great De-Risking: Why India’s Manufacturing Leap Demands a Supply Chain and Skills Revolution

The sudden, violent escalation of the Tehran-Tel Aviv conflict last month didn’t just rattle diplomatic circles—it choked the Strait of Hormuz in a grinding naval blockade. By this June of 2026, the fragile myth of frictionless, borderless trade has lay shattered. What we are witnessing is a series of economic shockwaves ripping through global energy and crop markets. In New Delhi, the mood is one of controlled panic. Emergency cabinet sessions convened earlier this month have scrambled to plug immediate farming deficits, while Dalal Street’s trading floors vibrate with the nervous energy of domestic markets pricing in prolonged chaos.

This blockade strikes at the jugular of global food security, threatening 35% to 50% of the world’s urea exports. It is a bitter pill for Indian policymakers: the dream of absolute self-sufficiency is dead. At the same time, Brent Crude has breached the $110-a-barrel mark, threatening to squeeze industrial margins to the bone. India’s aggressive, years-long sprint to build out solar capacity and nuclear grid buffers has offered some cover, but the government has still been forced to crack open its strategic petroleum reserves to keep factory wheels turning.

The year 2026 has shown that the very scaffolding of global trade is undergoing a violent, structural realignment. With the World Trade Organization (WTO) and the United Nations increasingly sidelined by unilateral manoeuvres, international commerce is being carved into regional trade blocs and “friendshored” networks. For India, which stands today precisely where China stood two decades ago—teeming with growth drivers, a massive workforce, and expanding industrial ambitions—navigating this fractured landscape requires a rapid transition from simple assembly to deep technological and human capital development.

The Fertilizer Crisis: A Case Study in Vulnerability

To see why this “Great De-Risking” is an existential battle rather than a dry academic exercise, look at the soil. The crisis currently gripping India’s agrarian heartland is a stark, mud-spattered proof of concept for why the old trade regime is broken.

Despite years of incremental progress, India’s exposure to external nutrient shocks remains dangerously high:

- Urea: Even with domestic manufacturing ramping up, India still relies on imports to cover 20% of its urea needs.

- Di-ammonium Phosphate (DAP): A severe domestic shortage of rock phosphate forces India to import a staggering 50% to 90% of its DAP.

- Muriate of Potash (MoP): Because the subcontinent lacks any mineable potash reserves, India remains 100% import-dependent on Russia and Belarus.

This crushing dependence on foreign nutrients has caused the state’s fertilizer subsidy bill to balloon to an eye-watering, unsustainable ₹1.86 lakh crore in FY26.

Breaking this loop requires India to borrow a page from China’s playbook, specifically its aggressive “zero growth of fertiliser use” policy. This means leaning hard into precision agriculture, bio-alternatives, and aggressive soil restoration—not just to save the treasury, but to insulate the food supply from foreign chokepoints. If agricultural shocks prove that raw material vulnerability can bring a nation to its knees, the lesson applies tenfold to the digital age’s “new oil”: critical minerals.

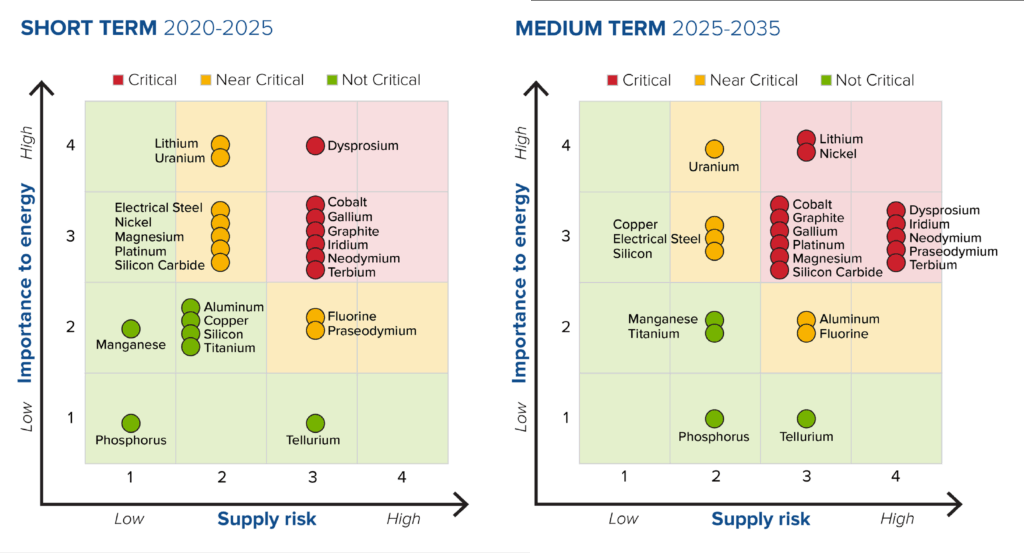

The Critical Mineral Scramble: The “New Oil” of Geopolitics

In the mining pits and boardroom offices, 2026 has marked a definitive shift. Critical minerals—the lithium, cobalt, nickel, graphite, and rare earths that feed our energy grids, defence systems, and silicon chips—are no longer treated as mere commodities. They are national security assets. The old laissez-faire regulatory approach has been buried under a new era of state-directed private partnerships.

This shift is born of a cold mathematical reality: the global supply chain for these resources is a monopoly.

Key Takeaway: By 2035, China is projected to refine over 60% of the world’s lithium and cobalt, and control approximately 80% of battery-grade graphite and rare earth elements.

Even as China’s rare earth exports ticked up 2.2% to 25,378 tonnes during the first five months of 2026, Beijing’s power to flip the switch and starve foreign markets of high-end magnets or agricultural inputs remains a massive geopolitical sword of Damocles.

India isn’t sitting on its hands. Its newly minted National Critical Minerals Mission (NCMM), backed by a ₹16,300 crore outlay and an anticipated ₹18,000 crore in public sector investments, is a frantic bid to construct a secure domestic pipeline. By utilizing Khanij Bidesh India Limited (KABIL) for overseas acquisitions and leveraging alliances like the Quad’s Critical and Emerging Technologies Working Group, New Delhi is scrambling to lock down the raw inputs that power modern battery chemistries and advanced hardware.

Dismantling the “Assembly Line” Paradox

For years, skeptics have dismissed India’s hardware boom as a hollow parlor trick—a glorified Chinese screwdriver industry where foreign components are shipped in, snapped together, and exported to dodge Western tariffs. While this transactional phase mirrors China’s early steps on the global stage, India is actively rewriting the script.

In the high-stakes “China+1” sweepstakes, India isn’t running in a vacuum. Vietnam dominates low-margin gadgets, Mexico rides its direct geographic highway to the US, and Poland has quietly become the battery heart of Europe. But India is playing a different game, pairing its massive domestic consumer market with aggressive supply-chain localisation.

Look at the hard macroeconomic data from early 2026:

- The Index of Industrial Production (IIP) expanded by 4.1% year-on-year in March 2026, anchored by a 4.3% rise in manufacturing and a 5.5% jump in mining.

- The HSBC India Manufacturing Purchasing Managers’ Index (PMI) printed a strong 53.9 in March 2026, signalling robust, continuous expansion.

- India’s Production-Linked Incentive (PLI) scheme, spanning 14 sectors with a committed $24 billion (INR 1.97 lakh crore), is successfully pulling advanced technology transfers into the country.

This maturation isn’t just theoretical; it is showing up on corporate balance sheets. In May 2026, home-grown electronics manufacturing services player Syrma SGS Technology posted a consolidated net profit of ₹119 crore for Q4 FY26. Its exports surged 41% to cross ₹1,200 crore—handily beating internal targets despite the West Asian maritime chaos and tariff volatility in the US.

At the same time, deep tech localisation is reaching critical security sectors. Earlier this month, defence tech pioneer Shield AI expanded its footprint in the country by executing a comprehensive transfer of technology for its V-BAT UAS (unmanned aerial systems), laying the groundwork for a fully indigenous production line on Indian soil.

Navigating the Tariff War and Trade Blocs

The global trading floor remains a volatile, knife-edge arena. Following a landmark US Supreme Court ruling in early 2026, the Trump administration slapped a 10% across-the-board tariff bridge on February 25, 2026, keeping the pressure on Beijing. While this trade war has accelerated “China+1” sourcing, any sudden thaw between Washington and Beijing could instantly erode India’s temporary cost advantages.

To insulate itself, New Delhi is actively hunting for alternative export markets. The newly signed India-UK FTA serves as a vital strategic counterweight. It grants zero-duty entry for Indian electronics—including smartphones, fiber optic lines, and power inverters—while offering British clean-tech and advanced engineering firms a direct gateway to India’s burgeoning middle class.

| Strategic Sector | Key Vulnerability (2026 Reality) | Policy & Market Mitigation Pathway |

|---|---|---|

| Electronics & Semiconductors | • Heavy reliance on Chinese components • Tariff volatility (e.g., US Feb 2026 tariffs) | • Semicon 2.0 (chip design focus) • PLI Scheme ($24B committed) • Recently ratified India-UK FTA |

| Critical Minerals | • China’s processing dominance • Rare earth export curbs | • National Critical Minerals Mission • Bilateral KABIL acquisitions • Quad mineral alliances |

| Agriculture & Chemicals | • Strait of Hormuz blockade • Ballooning subsidies (₹1.86T in FY26) | • Transition to precision agriculture • Domestic nano-urea scale-up • Import hub diversification |

| Advanced Defense Tech | • Historically slow indigenous R&D cycles • Lack of deep IP transfer | • Strategic tech transfers (e.g., Shield AI’s V-BAT UAS) • Private defense-tech integration |

The Silicon Bottleneck: Transitioning to Semicon 2.0

Building a real industrial powerhouse means moving past simple assembly and climbing into high-margin chip design and fabrication equipment. On June 3, 2026, the Indian government greenlit Semicon 2.0. This next phase shifts the focus from basic packaging to chip design, semiconductor manufacturing equipment, and the broader materials ecosystem.

By focusing on the complex chemistry and specialised machinery needed for fabrication, India hopes to shield its domestic electronics ecosystem from sudden supply shocks.

This effort is backed by a massive overhaul of the country’s physical transit network. India’s position on the World Bank Logistics Performance Index rose to 38th—a massive leap driven by major infrastructure milestones, most notably the Western Dedicated Freight Corridor (DFC), which became fully operational in early 2026. The Western DFC has dramatically cut shipping times between northern industrial hubs and western ports, stripping away the logistical friction of moving high-value goods.

Bridging the Skills and ESG Talent Deficit

Yet, India’s grand industrial plans will ultimately live or die on the factory floor and in the R&D labs. The SHRM India Skill Intelligence Report 2026 has exposed a massive disconnect between what modern factories need and what the domestic workforce can actually do:

- 41% of organisations report a massive talent gap in Green and Environmental, Social, and Governance (ESG) capabilities.

- Only 1 in 14 organisations qualifies as “advanced” in ESG talent capability, even as global buyers demand strict carbon accounting.

- 60% of Learning & Development (L&D) budgets remain locked in passive, digital self-paced or classroom instruction, rather than hands-on, high-end technical training.

If India wants to match the legendary manufacturing precision of Germany or Japan, its businesses must stop treating training as a line-item expense and start viewing it as a capital asset. The lack of a unified Vocational Education and Training Act—akin to the frameworks in Germany or China—remains a major systemic bottleneck, preventing workers from moving fluidly between trade schools and formal university degrees.

The Strategic Imperative

The volatile realities of 2026 have proven that geopolitical risk isn’t some rare black swan event; it’s a permanent cost of doing business. For India to truly cement its position as a global manufacturing giant, it must secure its supply chains through mineral alliances, drive deep IP localisation under Semicon 2.0, and completely overhaul its vocational training systems. Moving from a low-cost assembly plant to a self-sufficient, high-tech industrial power is no longer just an ambitious goal—it is a matter of national survival.

Summary of Key Takeaways

- Geopolitical shocks in mid-2026 have shattered illusions of free trade, forcing India to pivot from assembly to strategic supply chain resilience.

- Backed by the $24B PLI scheme and Semicon 2.0, India is localising advanced technology despite intense competition from Vietnam and Mexico.

- Long-term sovereignty requires bridging a 41% ESG skills deficit and securing critical mineral corridors.