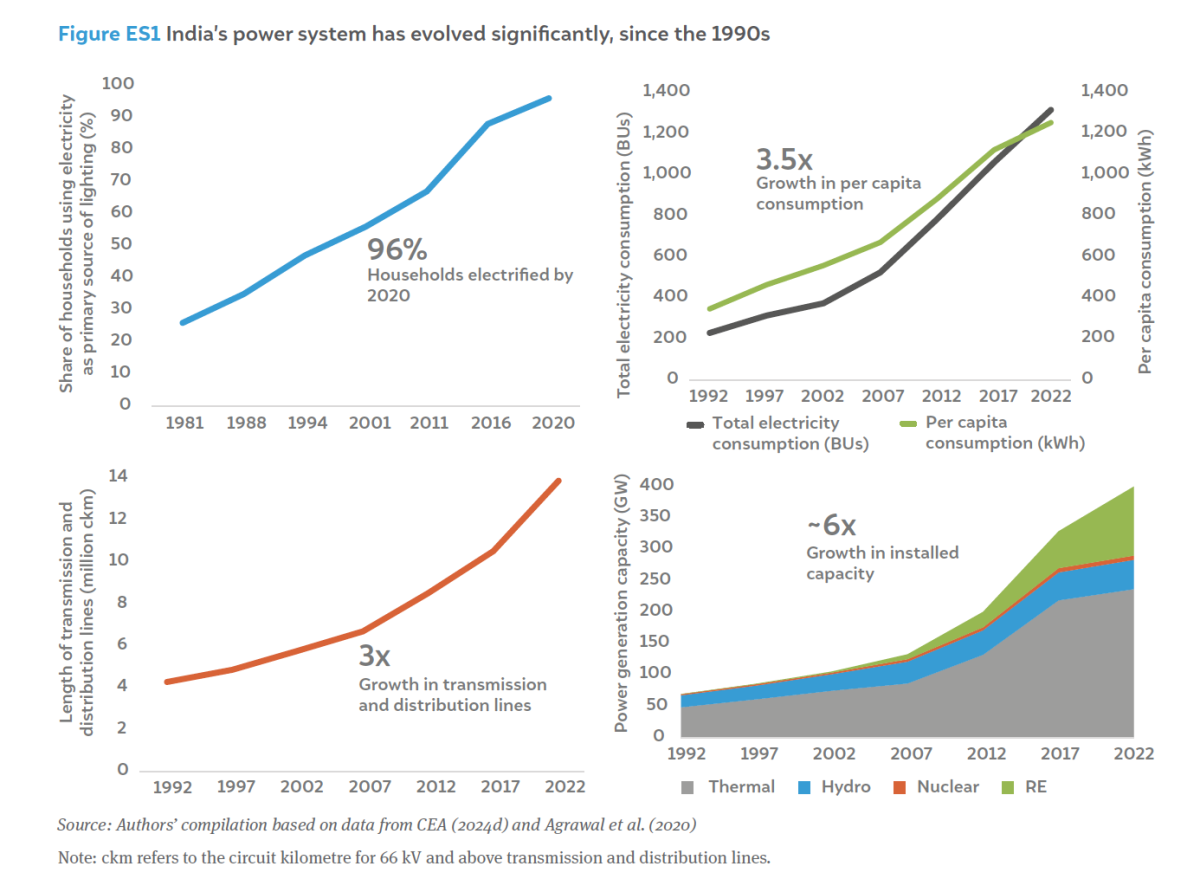

The Gas Gap: How Geopolitical Turmoil is Choking India’s Green Energy Surge

By late 2025, India’s green energy crusade hit a wall of its own making. Even as the nation obliterated records for renewable installations, it was simultaneously forced to dump the very electrons it had spent billions to harvest. Between May and December 2025, the country effectively tossed 2.3 Terawatt-hours (TWh) of solar juice into the void—a phantom loss worth somewhere between $63 million and $76 million. On paper, 2.3 TWh is a mere 1.8% of total solar output, but that average is a lie. It masks the chaos in solar hubs like Rajasthan and Tamil Nadu, where localized curtailment rates frequently screamed into double digits. As we lurch into 2026, the paradox is sharpening: India is on track to be the world’s second-largest solar market, yet it is haunted by a grid that simply cannot swallow the surge.

By 2026, India’s renewable energy ambitions are facing an unexpected and formidable adversary: a global natural gas shortage fueled by the escalating Middle East crisis. While the nation continues to break records for solar and wind installations, the grid is increasingly unable to absorb this power. The primary culprit is the loss of “peaking” flexibility—a direct result of the volatility in the global LNG market.Research Image

The 2025 Prelude: A System at its Breaking Point

The 2025 bleed wasn’t a fluke. It was the grid gasping for air. As solar penetration went vertical, system operators had to lean heavily on “Emergency TRAS-down” (Tertiary Reserve Ancillary Services). Think of TRAS-down as the grid’s emergency brake—a panicked manual or semi-automated shout from the National Load Despatch Centre (NLDC) telling generators to kill their output before the frequency spikes and the lights go out.

The “unexpectedly weak daytime demand” that triggered this was a perfect storm of bad luck and shifting economics. A freakishly mild monsoon season killed the expected cooling loads, while energy-intensive factories, spooked by price volatility, dialed back their operations right when the sun was highest. The result? A massive surplus the grid was never built to digest.

“Relying on renewables to provide flexibility by simply switching them off is an inefficient system response. It represents a massive economic drain and a missed opportunity for decarbonization.”

2026: The Convergence of Three Crises

If 2025 was about growing pains, 2026 is about a structural heart attack. Three distinct pressures are turning occasional curtailment into a permanent crisis.

1. The Peaking Power Vacuum

Gas plants are the “scalpels” of the power world. They can ramp up or down in minutes, balancing the solar curve with precision. But that tool is now blunt. The Middle East crisis, and the resulting chaos in Red Sea shipping lanes, has turned the Global LNG market into a gambling den. With India tethered to expensive spot-market gas, many plants have gone into “cold standby.” The grid has lost its most agile defense just as it needs it most.

2. The “Coal Anchor” Effect

There is a ghost in the machine: the memory of the 2022 coal shortages. To avoid a repeat, the government has chained the grid to a “Security of Supply” mandate. Coal plants are forced to maintain high technical minimums. While a modern supercritical plant can technically “back down” to 55% of its Plant Load Factor (PLF), they aren’t allowed to. Operators keep the boilers roaring to ensure they can hit the evening peak, creating a “base-load floor” that physically crowds out solar power during the day. We are burning coal to keep plants ready, while throwing away free sunlight.

3. The Infrastructure Lag

The Inter-State Green Energy Corridor (GEC) is losing its race against the sun. There is a ₹9.12 lakh crore investment on the books to build 33.25 GW of High Voltage Direct Current (HVDC) links by 2032, but wires don’t grow as fast as panels. A transmission line takes three to five years to clear red tape and construction; a solar park takes fourteen months. In 2026, this “velocity gap” is no longer a footnote—it is the primary bottleneck.

The Peaking Power Vacuum: Why the Middle East Matters

Natural gas plants are the “scalpels” of the power grid. Unlike massive coal boilers, gas turbines can ramp up or down in minutes, providing the surgical precision needed to balance the inherent intermittency of solar and wind. However, this critical balancing tool has been neutralized.

- The Red Sea Bottleneck: Chaos in Middle Eastern shipping lanes has turned the Global LNG market into a high-stakes gambling den.

- The Price Spike: With India tethered to expensive spot-market gas, many gas-based peaking plants have been forced into “cold standby.”

- The Result: Without affordable gas to smooth out the fluctuations of the sun and wind, grid operators are left with only one crude option: Curtailment. They are simply switching off renewable plants to prevent grid frequency spikes.

Comparative Impact: Flexibility vs. Constraints (2026 Outlook)

| Factor | Status | Impact on Curtailment |

|---|---|---|

| Gas-Based Power | Crippled by Red Sea/LNG volatility | Severe Increase: Loss of fast-ramping support forces more solar/wind to be switched off. |

| Middle East Crisis | High shipping risk/Price volatility | Direct Cause: Makes the “balancing act” of the grid economically unviable. |

| Coal Flexibility | Mandated high-load operation | Negative: Fills the “base-load floor,” leaving no room for midday solar surges. |

| Solar/Wind Growth | 50 GW added in 14 months | Pressure: Rapid growth exceeds the grid’s ability to compensate without gas. |

| Battery Storage | Costs at $134/kWh | Mitigating: The only viable alternative to gas, but currently under-deployed. |

The Silicon Safety Net: Beyond the Coal-First Mindset

The math is blunt: India cannot build its way out of this with more panels alone. We need a “flexibility-first” architecture. Battery Energy Storage Systems (BESS) and Pumped Hydro are the only real exits from the curtailment trap. As of early 2026, our BESS capacity is a drop in the ocean compared to the 230 GWh required by 2030.

The good news? The price of silicon is finally catching up to the reality of the grid. With BESS costs hitting $134/kWh, storage is no longer a “future tech” luxury; it’s a fiscal necessity to stop wasting $76 million a year. But batteries aren’t a silver bullet. We need aggressive Demand-Side Management (DSM) to bribe factories and farmers to use power when the sun is out, and a more fluid inter-state trading system to shunt power from the scorching West to the hungry East.

India’s transition has reached a tipping point. It’s no longer about adding raw megawatts; it’s about the intelligence to manage them. Without a silicon safety net, the solar surge will simply overwhelm the very grid it was meant to save.

The Path Forward: Breaking the Gas Dependency

The math is clear: India cannot solve its curtailment crisis with more panels alone. The Middle East crisis has proven that relying on imported gas for grid flexibility is a strategic vulnerability. To stop the “Green Bleed,” the focus must shift:

- Aggressive BESS Deployment: With battery costs hitting $134/kWh, storage must replace gas as the grid’s primary “scalpel.”

- Demand-Side Management: Shifting industrial and agricultural loads to daylight hours to consume solar power at the source.

- Coal Modernization: Incentivizing coal plants to operate with greater flexibility to allow renewables to take priority during peak production.

Without a transition toward a “flexibility-first” grid that accounts for the permanent loss of cheap gas, India’s record-breaking solar and wind surge will continue to hit a wall of its own making.