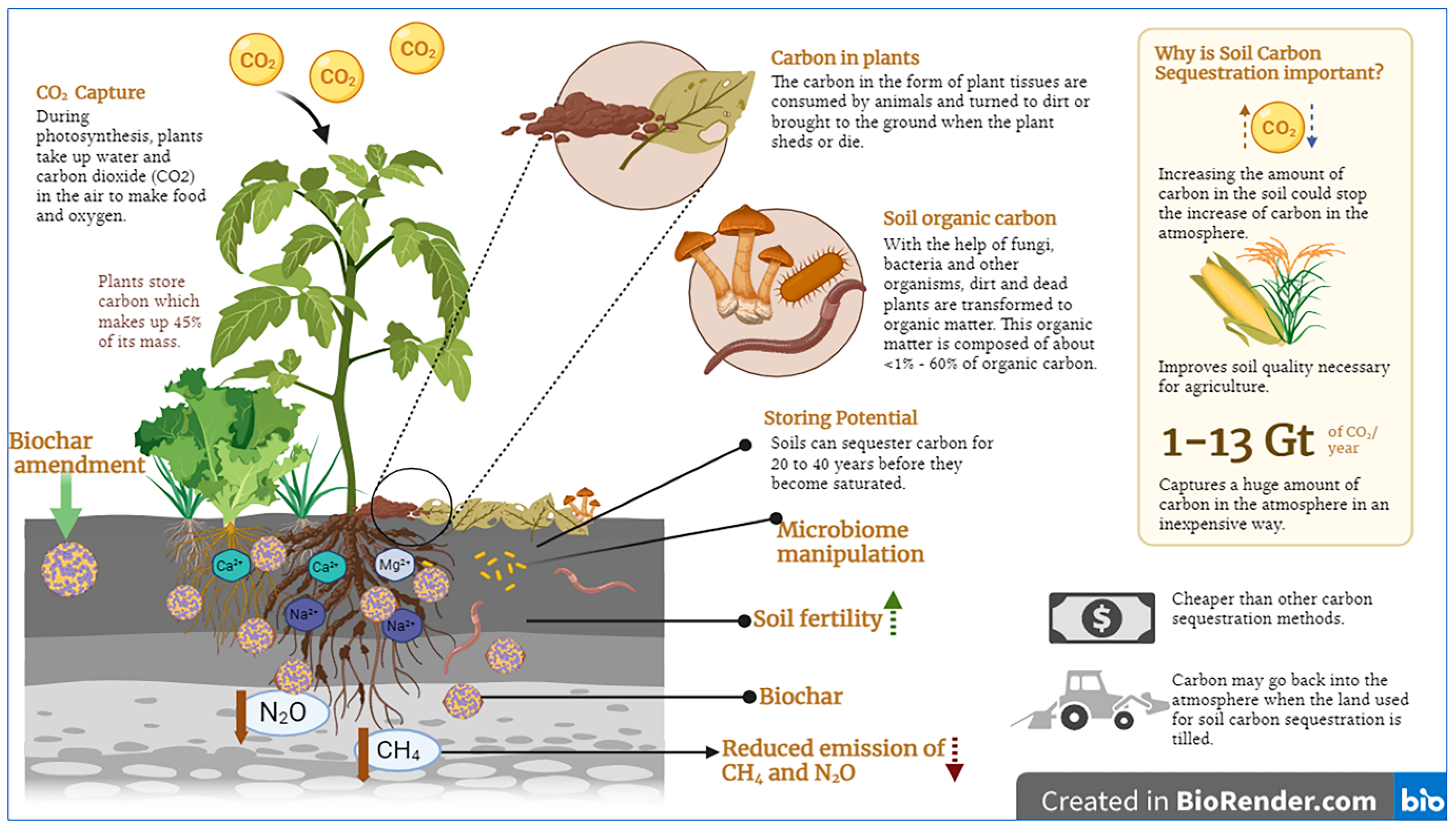

The Biochar Blind Spot: Saving the Climate, Losing the Soil

The financial forecasts are intoxicating: the biochar industry is expected to balloon from USD 2.2 billion in 2024 to a staggering USD 6.3 billion by 2033. Yet, beneath this veneer of exponential growth, a dangerous disconnect is festering. Today’s large-scale industrial projects—bankrolled by tech giants and multinational carbon developers—are being engineered to satisfy the sterile, high-threshold appetites of voluntary carbon markets (VCMs). The problem? This optimization often ignores the very person who makes the technology viable in the first place: the smallholder farmer.

The friction on the ground is palpable. If biochar is treated as nothing more than a sequestered carbon commodity—a line item on a digital ledger in London or New York—the industrial bubble will eventually pop. For a grower in the tropics or the American Great Plains, biochar isn’t a financial derivative; it is the difference between a failed harvest and the resilience of a grain fill during a savage drought.

The Industrial Disconnect: Carbon Credits vs. Soil Health

The current corporate trajectory leans toward massive, centralized production hubs. It is a model built to appease the rigorous Monitoring, Reporting, and Verification (MRV) protocols of gatekeepers like Verra or Puro.earth. These standards prioritize high-permanence thresholds and massive tonnage, often incentivizing “pure” carbon over “functional” carbon.

“The responsibility of a biochar project developer often ends when the char is delivered. But for the farmer, that is where the challenge begins. Without immediate nutritional value, raw biochar is frequently viewed as an additional cost—a luxury compared to the immediate, albeit fleeting, growth spike provided by subsidized urea.”

This creates a massive economic wall. In many emerging economies, governments heavily subsidize synthetic fertilizers like urea to keep food prices stable. Raw biochar, by contrast, is often “nutritionally inert.” Its high carbon-to-nitrogen (C:N) ratio and porous architecture can actually suck existing nitrogen out of the soil in the short term, a phenomenon known as “nitrogen robbery” that leads to visible yield drops. Unless we focus on Nutrient-Enhanced Biochar (NEB)—charging the char with nutrients before application—farmers will likely stick with the subsidized certainty of chemicals.

Comparative Analysis: Industrial vs. On-Farm Biochar Models

| Feature | Industrial/Carbon-Centric Model | Farmer-First/Smallholder Model |

|---|---|---|

| Primary Goal | Carbon Sequestration Credits (CORCs) | Soil Fertility & Yield Resilience |

| Feedstock Source | Centralized/Hauled Timber & Waste | On-farm Residues (Rice husk, Betel nut) |

| Cost to Farmer | High (Market Price + Logistical Overhead) | Low (Self-produced or Cooperative-led) |

| Knowledge Gap | High (Top-down delivery, minimal training) | Low (Farmer-led learning & TLUD kilns) |

| Economic Viability | Dependent on Fluctuation of Credit Pricing | Dependent on Yield Increase (~15% avg.) |

| Mechanisms | High-heat Pyrolysis (Industrial Grade) | TLUD Kilns (Low-cost, Decentralized) |

Silicon Valley is Betting Billions on India’s ‘Black Gold’

We are looking at a CDR market poised to scream past $10 billion by 2030. India, with its endless supply of waste and new capacity to cook it at scale, has become the primary vault for the world’s climate billions.

The Multi-Million Tonne Stakes: A Strategic Comparison

The market for Durable Carbon Removal (CDR) has moved past the “experimental” phase. It’s now an industrial requirement. While old-school nature-based solutions—like planting trees—constantly face “leakage” risks (think forest fires or illegal logging), biochar is different. It’s a geologically stable, measurable sink. Google and Microsoft have already tapped Varaha as a Tier-1 partner, signaling a massive pivot toward hardware-heavy, science-first removal.

| Feature | Google’s Strategic Bet (2025) | Microsoft’s Industrial Expansion (2026) |

|---|---|---|

| Transaction Volume | 100,000 tonnes of CDR credits | 2 million+ tonnes projected (15 years) |

| Estimated Deal Value | ~$12M – $16M (at $120–$160/tonne) | ~$250M+ total contract lifecycle |

| Infrastructure | 6 Industrial Biochar Reactors | 18 Industrial Gasification Reactors |

| Primary Feedstock | Invasive Mesquite (Prosopis juliflora) | Cotton Residue (Gossypium) |

| Key Objective | Biodiversity & Grassland Restoration | Air Quality & Soil Health in Cotton Belts |

| Operational Model | Distributed “Hub-and-Spoke” | Integrated Industrial Deployment |

The Adoption Bottleneck: Knowledge, Labor, and Logistics

Despite the glossy brochures, a “knowledge poverty” remains the industry’s Achilles’ heel. Data synthesized from FAO and World Bank agricultural surveys reveals that roughly 63% of smallholder farmers lack even a basic grasp of the pyrolysis process, while 71% remain unaware of how biochar fundamentally alters soil physics. This isn’t just a communication failure; it’s a direct threat to the 10.9% CAGR the industry expects.

Then there is the sheer physics of the stuff. Biochar is bulky, light, and incredibly dusty. Moving it from a centralized factory to a remote farm adds a “logistics tax” that can effectively double the price per ton. Moreover, the back-breaking labor required to till biochar into the earth—often done by hand in smallholder contexts—is a dealbreaker unless the yield benefits are immediate and undeniable.

However, when biochar is woven into a closed-loop system, the math changes. University trials across Southeast Asia and East Africa show that co-composting—mixing 5–10% biochar into raw organic compost—acts like a “soil battery.”

It preserves nutrients that would otherwise off-gas and slashes the need for expensive, imported fertilizers.

Why Smallholders are the True Market Drivers:

- Drought Performance: Biochar boosts the soil’s Water Holding Capacity (WHC). When the rains fail, biochar-treated plots often become the only green patches in a brown landscape.

- Yield Multipliers: In trials focused on high-value coffee and maize, yield jumps of 1 to 3 metric tons per hectare have been documented when biochar is paired with organic inputs.

- Waste Valorization: Rather than burning crop waste in open fields—choking the air with smoke—farmers can use TLUD (Top-Lit Up-Draft) kilns. These simple, low-cost units turn waste into wealth with virtually no emissions.

The Policy Shift: From Credits to Incentives

In the U.S., the USDA’s EQIP Practice 336 (Soil Carbon Amendment) represents a rare moment of policy clarity. By providing financial help to growers for biochar application, the government is effectively de-risking the “startup cost” of regenerating soil.

But for the global South—where the Asia-Pacific region holds a 40.26% volume share of the market—we cannot wait for the VCMs to mature. We need “Blended Finance”: a mix of private carbon capital and public grants to cushion the transition for the world’s most vulnerable farmers.

Key Economic Insight: Financial feasibility is highest when the production chain is vertically integrated. Integrated business scenarios—combining forest management, local biochar production, and biomass energy sales—show significantly higher Net Present Value (NPV) and payback periods reduced by up to 40% compared to standalone sequestration projects.

The Pathway Forward: Shifting the Narrative

If industrial titans continue to hunt for carbon credits while ignoring the “urea-cost comparison,” they are building an industry on shifting sands. To build a market that lasts, the pivot must rest on three pillars:

- Blended Finance: Funneling carbon credit revenue directly into subsidies for farmer-level distribution and application gear.

- Community Kiln Models: Moving away from “mega-plants” toward cooperative-managed facilities that “charge” biochar with local manure or urine.

- Nutrient-Enhanced Biochar (NEB): Reimagining the product not as “raw charcoal,” but as a high-performance “bio-organo-mineral” fertilizer that gives farmers the NPK spike they need.

The takeaway for the industrial sector is simple: Biochar isn’t just a tool for cooling the planet; it’s a tool for resilient livelihoods. If we don’t put the farmer first, those billions in projected market value will remain nothing more than a paper promise.

“Biochar’s survival depends on prioritizing soil resilience over speculative carbon markets.

- Industrial projects must pivot to Nutrient-Enhanced Biochar to compete with subsidized urea.

- Decentralized TLUD kiln models and Blended Finance are essential to bridge the 71% knowledge gap.

- Success requires viewing the farmer as a partner, not just a carbon sink.”